Housing may be recovering, but it has not done so in a manner that is beneficial for the middle class.

There can be little doubt that the U.S. housing market is in recovery – home prices reversed track in 2013, and have risen steadily since then; construction is on the rebound; and most promising of all, foreclosures and delinquencies continue to improve with each passing month.

However, this housing recovery is not one that has benefited all consumers equally, and new research from Redfin recently counted the ways that the middle class continues to be shut out from the fruits of the current housing market.

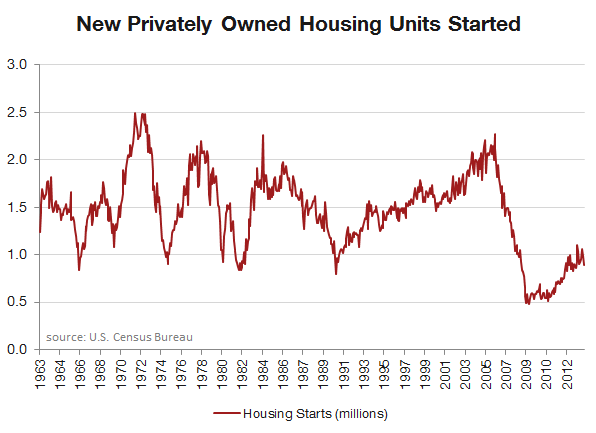

1. Lagging New Construction – We know, we just mentioned that construction is on the rebound, but such a statement comes with a significant caveat. Even with construction’s recent gains, overall construction is still hovering near all-time lows, and the homes that builders are constructing are larger, more expensive and outside the reach of the middle class. Why? As we continue to point out, builders are gearing their product to wealthier consumers, aka the absolute safest target market in housing today.

Here’s a great graph from Redfin on the lagging construction numbers:

2. Unfair Competition – Even among the housing stock that the middle class can afford, the competition has been fierce, and, often, unfair. Not only have consumers competed with all-cash buyers, who skate through the homebuying process (and the time-consuming post-boom underwriting procedures), but they’ve also had to grapple with investors, who have bought homes in bulk for the purpose of renting them out. Here’s a remarkable stat – for homes priced $130,000 or less in July, 61 percent of sales were all-cash, up from 56 percent in 2011.

3. The Market Has Left Them Behind – On top of lagging supply and unfair competition, the middle class must also deal with a housing market that has left them behind price-wise, and in a hurry. According to Redfin stats, homes in the housing market’s “middle range” ran from $1550,00 to $429,000 in July 2014, which was, on account of low inventory and strong demand from investors and wealthier consumers, 36.6 percent higher than the middle range of July 2011. Here in Chicagoland, the price range of $130,000 to $385,900 was up 17.9 percent (click here for other metro area ranges).

4. Financial Traps – Finally, even for middle class consumers who do own a home, it’s not as though they have many options for selling their home. As many as 35 percent of current homeowners cannot list their homes either because of low equity or “rate lock-ins,” meaning they refinanced at a historically low rate and cannot purchase a new home at a similar rate. Such constraints not only limit options for middle class homeowners – they also limit the possible inventory for fellow middle class consumers looking to buy.

Overall, the more you look at it, the more housing’s trends in the post-bubble marketplace mirror that of other sectors in the economy, where price and inventory appeal to a strengthening upper class and a disappearing middle.